|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|||||||||||||

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

|

"There are two kinds of forecasters: Those who don't know, and those who don't know they don't know'' John Kenneth Galbraith (Wall Street Journal, January 22, 1993) “There are known

knowns; there are things that we know that we know. We also know there are

known unknowns; that is to say we know there are some things we do not know. But there are also

unknown unknowns, the ones we don't know we don't know” Donald

Rumsfeld Forecasting Science and Theory of Forecasting Forecasting

is a kind of decision making for defining the most expected scenario from

alternatives of future prospects. Although it is not explicitly mentioned,

many of our decisions are forecasting the future of a system, organization,

human behavior etc. Forecasting is one of the most used functions of human

recognition which works unconsciously. We predict arrival time, departure

time, cost of daily consumables and behavior of a friend and so on. However,

there are some popular forecasts which usually have particular media coverage

such as weather forecasts, economic forecasts and the story of fortune

tellers based on a magical crystal ball! The

reputation of forecasting is deteriorated with improper practices and poor

knowledge about the theory of forecasting. There are several common

misconceptions about forecasting and the method of forecasting process.

Therefore, it is strongly needed to illustrate what forecasting is and how it

works. Exordium: Philosophy of Forecasting Forecasting

is not a new topic, and it is frequently discussed with the physical

phenomena. One of the critical questions about the forecasting is

predictability debate. Before approaching to forecast, people need to clarify

whether it is achievable. In the similar circumstance, the difference between

the nature (physics) and human make a strong impact on our perception of

forecasting. Human sciences e.g. economics are subject to the uncertainty of

mankind which requires an extraordinary effort for forecasting. Physical

phenomena are usually based on robust, clear and repetitive rules. One can

easily predict destiny of a ball if it is released from a table: It drops to

floor. We are unconsciously aware of several physical rules including

gravity. However, when it comes to a complex problem such weather

forecasting, there is a huge number of forces and systems working together.

In such cases, we are unable to make a precise and error-free forecast. On

the other hand, the movements of earth, moon, sun and most part of astronomic

motion can be predicted precisely even in seconds of time. Economic

phenomena as the most popular field for forecasters has somewhat different

dynamics. In the core of the problem, we, human, exist, and our nature is

quite complicated. The models of our behavior can change every day. We may

dislike something today which we liked it yesterday. Therefore, most of the

econometric models need to be re-estimated and re-thought frequently. No

model can serve for several years. The use

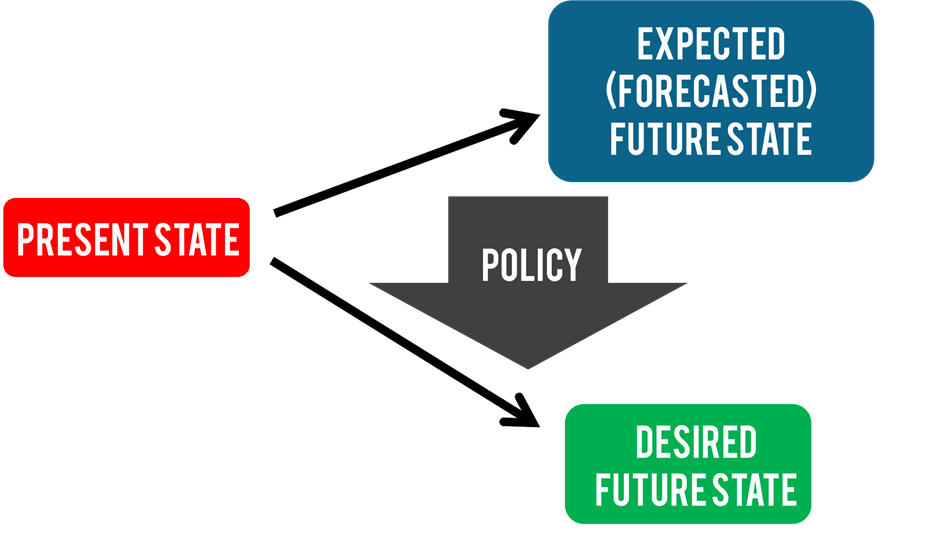

of forecasts and the state shift are some other critical topics. Forecasts

are usually required for developing broader policies or strategies in micro

level. Based on the forecast, decision makers define a policy to achieve a

desired outcome. Therefore, policies are employed for changing the direction

of a phenomena from the expected (non-intervention) future state to desired

future state. The major function of policy here is shifting between states by

using policy/strategy instruments.

As a

result of policy actions (intervention), the nature of phenomena changes, and

now it is not same as estimated at the time of forecasting. If policies are

somewhat successful, forecasted future state will not become a reality. If

someone criticizes the failure of the forecast, that would be ignorance of

the function of a forecast. Unless a forecast is kept exclusive for a person or

a small group of people, future state will always change, and it will be

replaced with a new one. The theory of information asymmetry emphasizes that

if an information is hold by exclusive users, then that will create an

advantage for them. Based on this, we can roughly say that a publicly known

forecast probably fails since decision makers replace their position and

direction. In addition to that, if most of the decision makers are familiar

with the state-of-art forecasting methods, they will probably conclude

similar predictions which in turn causes similar strategies. Finally,

forecasts will fail even in exclusive terms since the method is common and

symmetrical. That is the current situation in the financial markets. Although

forecasts are exclusive, methods are well known, and even many trader

companies employ quants with PhDs from Harvard or MIT to find a less known

way of forecasting. When

human action is in the problem, there is no straight and accurate way of

prediction whether a forecaster runs complex mathematical functions and

simulations with an extraordinary programming talent. Assumptions behind

the classical forecasting methods The

major assumptions behind forecasts are the repetitive nature of history and

the stationary nature of decision makers. The recursive history perspective

is very old topic, and it is one of the main themes of Muqaddimah

(Ibn Khaldun) which is the first written publication of the scientific method

to social sciences and the philosophy of history. In modern times, Peter Turchin extended and mathematically presented the theory,

and even he developed models of historical dynamics. Cliodynamics

is branch of history dealing with the mathematical modeling of historical

fluctuations and metamorphosis. According to the theory, the most part of the

history is a kind of cyclic movement while names, titles or instruments are

changed. For example, civilization has a cyclic behavior and every

civilization movements and developed empires have a life span from birth to

mature and death. The

current business cycle theory also supports the theory of recursive history

and both macro and micro level economic systems are subject to cycles of

upturns and downturns i.e. recovery and recession. However, the vital point

of the theory is the size and schedule of cycles. Based on the recursive

history assumption, every forecaster deals with finding a proper method to

define particulars of coming cycles. For longer periods, forecasters study

long term cycles and for shorter terms they look for short term cycles. Another

critical assumption is the stationarity of decision makers which refers to

the identical reactions to identical impacts (Reader may confuse with the

rationality assumption which is a quite different matter and will be

discussed later). The recursive history assumption somewhat includes the

stationarity of decision makers. History repeats itself since decision makers

behave identically in addition to the identical circumstances. Under these

assumptions, we recognize the historical pattern and replicate it to find

future direction. From

the economic perspective, the utilization of decision making processes is a

common issue and it is known as rationality of decision maker. It is very

similar to the stationarity assumption with a slight difference. In

stationarity assumption, we assume that all economic agents behave

identically even when these selections and decisions are inadequate. If some

decision makers make faulty preferences, we assume that this faulty decision

will be repeated as well. However, rationality assumption is about the

finding the optimum decisions among a number of options in every cases.

Econometric models are usually based on rationality assumption which means

the economic agents of the intended marketplace rationally defined and

defines optimum economic preferences. Therefore, the proposed model is

estimated under the rational circumstances and the future state is expected

to be rationally managed. Based on these assumptions (many assumptions mean

it is probably impractical), history will repeat itself in the rational

people’s world. However, rationality assumption is strongly criticized in the

last few decades and the irrationality concept (also bounded rationality) is

a growing topic in the field. Why micro economic forecasts are usually inferior in

business practice? It is

related with the publicity of forecasts. As it is discussed in Exordium, the asymmetric information

refers to the possibility of arbitration in case of private market

intelligence. If an economic forecast is publicly available, every decision

makers consider this evidence and revise the direction of their investment.

Although macroeconomic and long term forecasts are able to predict cycles

roughly, micro-economic and short-term fluctuations are affected by the short

term position changes of agents. Once a forecast is publicly available, every

agent moves to a new position, and then the decision space of desired future

will dramatically change. From that time, the particulars of marketplace is

not same as it is assumed/estimated in the modelling stage. Although

the model delivers proper predictions, it will never be accurate since it is

common information. Many international organizations (e.g. World Bank, IMF)

publish macro-economic forecasts while it is very difficult to find publicly

available forecasts for industrial markets. Usually we pay charges for them

and we wish that a few people reach to these predictions. Otherwise they are

worthless and “inaccurate” as a result! Methods of Forecasting Forecasting

methods have two major divisions: Quantitative methods and qualitative

methods (i.e. objective vs. subjective). Econometric modeling, time series

analysis, neural networks and other methods of mathematical solutions are

quantitative methods, and they are very useful when there is a repetitive

nature. For example, seasonal time series methods are quite accurate for

prediction of ice-cream sales or the volume of harvest. However, they are

strictly limited to the historical pattern, and it is impossible to embed

pure subjective factors, expectations or political aspects. Therefore,

qualitative methods are utilized distinctly or in addition to the

quantitative methods. Judgmental forecasting is a typical subjective

forecasting method, and it is frequently used for exposing herd behavior and

other psychological trends. Expert guided adjustment of quantitative methods

is an alternative solution to gain advantages of both. Judgmental forecasts

are also limited to biases and heuristics of decision makers. For this

reason, a special care is needed to handle and manage judgmental forecasts. The use

of computer intelligence, neural network models and fuzzy sets for

uncertainty problem is a growing section of forecasting science, and these

methods contributes to the improvement of processes, randomness and

complexity (i.e. chaos systems). The existing literature has several good

applications of computer intelligence which are superior to the conventional

time series analysis and the orthodoxy of econometrics. Fundamentals of Forecasting In a

brief list, we may figure out some fundamental needs and common failures of

forecasting studies: (1) Data control and preparation: Stationarity control | Data transformation if

needed (2) Sampling (Partitioning): Defining the in-sample period for training

(estimation) and the post-sample period for real forecasting test (i.e.

testing period) (3) Benchmark Selection: Conventional methods and other potential competitors of the proposed

forecasting method should be selected as benchmark. Since this step is

subjective, one may intend to select inferior methods to highlight the

proposed one. A computer intelligence method should not only tested against

similar one, but it should also be compared with the conventional time series

methods. (4) Accuracy Metric Selection: There are several accuracy metrics used frequently

while they are quite biased (e.g. MAPE, RMSE). For example, Mean Absolute

Percentage Error (MAPE) is one of the most biased error metrics. Assume that

we have two actual value, 1 and 5, and then our model generates same

predictions for them, 3 and 3, which means same absolute error for both, 2

and 2. MAPE for these forecasts are |1-3|/1=2.0 (200%) and |5-3|/5=0.4 (40%).

Although absolute errors are same, MAPE metrics have a huge difference. If

forecasting model systematically predict less (undervalue), then we will find

it superior. Please be aware of illusion of accuracy gain. Mean Absolute

Scaled Error (MASE) is a relatively better choice for accuracy control. (5) Residual Control: Residuals should be checked against whether a remaining pattern

exists. A figure showing the residual series is usually enough for

illustrating the white noise control. White noise testing procedures (e.g.

serial correlation test) may also clarify whether residuals are really

irregular oscillations. Ethics of

Forecaster Forecasting methods and procedures are usually

subject to expert consultation, and there is a strong potential of unethical

use or presentation. Subjective selections and arbitrary preferences may help

to validate and rationalize the scholar’s work (self-serving bias), then the

outcome would not be useful and practical. By this way, forecasting study

turns to be an entertainment rather than a professional effort. Forecasters are strongly

encouraged to criticize their work and profession if they concern about the

practical meaning of their efforts.

|

|

||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Copyright Okan Duru©2014